Banking on Innovation

How FinTech is Disrupting the Financial Landscape and Challenging Traditional Banks

The proliferation of FinTech players in recent years has transformed the payment landscape for the better, thanks to technological advancements and regulatory changes. These companies have innovated across several FinTech subsectors, including payments, personal financial management, digital lending, and wealth management. Venture capital investments in the payments space alone have accounted for more than 40% of total investments in the US and 33% in MENA over the past five years. This abundance of capital pouring into innovation has created a sense of threat for incumbent financial institutions.

According to a Global Survey conducted by McKinsey, financial institutions that incorporate innovation into their strategies are six times more likely to succeed. However, FIs have been struggling to compete with FinTechs. Whether FinTechs represent opportunities or threats to FIs involves several factors to assess. Banks possess deep industry expertise and knowledge that new FinTech companies still need to gain. But, as they face unprecedented innovation from FinTechs, banks cite regulatory hurdles, lack of focus, and insufficient infrastructure as impediments.

Banks are built on legacy systems that have been prevalent for over 300 years. The average bank has 200,000 to 400,000 individual processes and services that are siloed. To implement a radical change, banks must undergo a cumbersome process to amend their infrastructure to obtain real-time data exchange and APIs. This process would require banks to unify all product offerings and apply data at the center point of all decision-making. Infrastructure modernization poses a risk to financial institutions as they do not want to compromise on customers’ data or experience along the way. While they can undertake some changes, banks cannot afford to fail on a large scale due to depositor and shareholder funds. Hence, incumbents are approaching the transition more progressively. In addition, banks “have a lot to lose.” Testing out new tech, especially with customers, could expose unproven processes to a bank’s customers, putting the business the bank is already conducting at risk. Simply put, if a bank already has a “profitable” relationship with its customers, why would it want to push the envelope and risk damaging that relationship? As a result, incumbents often hesitate to adopt new technologies and approaches and may only do so gradually and cautiously.

At the same time, the bar of customers’ expectations continues to rise. Within payments, customers are demanding the ability to conduct instantaneous fund transfers around the clock, all while experiencing speed, convenience, ubiquity, safety, and affordability. Due to their agility, FinTechs have been able to offer customer-centric services at increasingly cheaper and faster rates. FIs simply have not been able to keep pace.

So, what characteristics give FinTech companies an advantage over incumbent FIs in driving innovation? And where do more mature companies maintain competitive advantages over FinTechs?

FinTechs over FIs

FinTechs have a lean organizational structure that permits quicker and easier change.

FinTechs have a clear imperative to push boundaries and create products that are new to the market in order to gain market share in the first place.

FinTechs tend to have superior techniques for acquiring new customers in creative or low-cost ways.

FinTechs utilize data and technology to drive innovation and offer enhanced products and services that are more appealing to customers.

While banks have access to gold mines of customer data due to their longevity in business, FinTechs have the capability to leverage such data and deploy computing power to extract meaning and monetization.

Since the financial crisis, banks have encountered heightened regulatory compliance requirements, resulting in significant costs in terms of both capital and time needed for implementation. For example, increased regulatory oversight is estimated to cost the six largest US institutions around $70 billion per year. Meanwhile, in the MENA region, we’ve witnessed several governments implement reforms to strengthen their financial system and prevent future crises. For example, both the CBUAE and SAMA introduced new regulations to enhance the capital adequacy and liquidity of banks.

FinTech Disadvantages

Banks have deep industry expertise and knowledge that FinTechs lack. They are also licensed institutions that provide FinTechs with mandatory services such as the safeguarding of accounts.

Banks have well-developed business models around cross-selling and up-selling products to customers. This allows them to monetize in a variety of ways, ensuring positive & sustainable long-term unit economics.

Banks have been operating for a long period and have cultivated strong relationships with customers. Having a brick-and-mortar store helps create a personal and tangible relationship with clients.

FinTechs are not as highly regulated as banks and are predominantly middlemen within financial services. This triggers concerns regarding their long-term sustainability, especially during economic downturns.

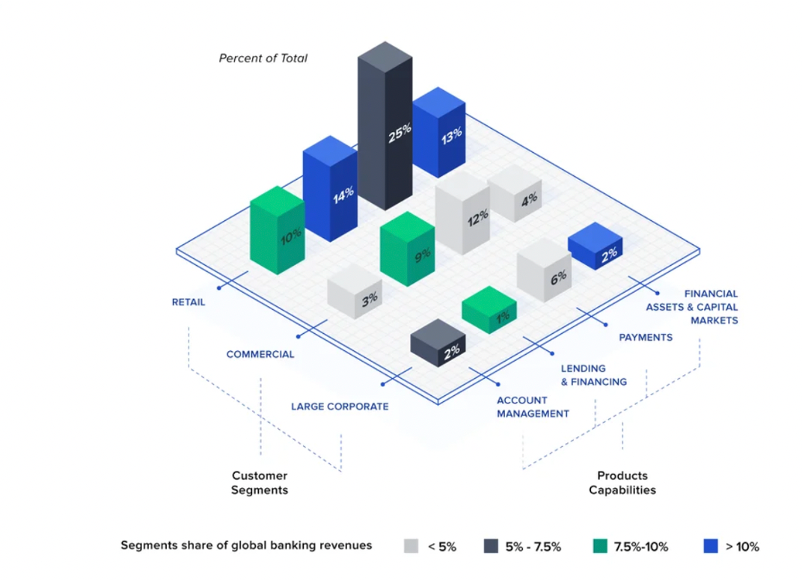

It is worth noting that FinTech companies do not compete with banks across all products and services. A report by McKinsey revealed that 62% of startups focus on retail banking while only 11% target large corporate banking. The following chart illustrates the product and customer focus of a sample of 350 FinTech startups to showcase where banks and FinTechs overlap in terms of products and services.

The majority of FinTech companies are currently focused on unbundling banks, which involves streamlining a product or service within the existing array of services offered by banks to enhance its potential. It is crucial to note that this does not imply that FinTechs will entirely overhaul the banking industry (at least not in the short term – in the long term, a “re-bundling” is all but inevitable for successful FinTechs). However, banks that do not innovate risk losing a substantial amount of market share in terms of both users and revenue.

Although banks have the capability to develop new products internally, many are choosing to collaborate with third-party platforms or invest in related players to accelerate innovation. In the US, for example, an estimated 63% of banks have established startup venture funds or accelerators, compared to just 7% that have created their own FinTech research and development (R&D) subsidiaries. Similarly, we’ve seen similar initiatives occurring in the Region, such as Arab Bank launching a FinTech-focused accelerator and the EGP 440 million fund led by Banque Misr, National Bank of Egypt, Banque du Caire, and Suez Canal Bank, among others. Those efforts are aimed at driving FinTech innovation and facilitating financial inclusion.

FinTech companies are bridging the gap between what traditional banks offer and what contemporary customers demand, serving as de facto R&D arms for the financial industry. The success of these banks heavily relies on their ability to collaborate with FinTech disruptors who are transforming the financial landscape. This collaboration is particularly crucial in the MENA region, where there is a significant unbanked population. Partnering with FinTechs presents a massive opportunity to promote financial inclusion and achieve a level of economic development that is comparable to that of the Western World.

This article way originally published on waya.media.

| A guest post by

|